Hedge Fund Mayhem, Preppy Style

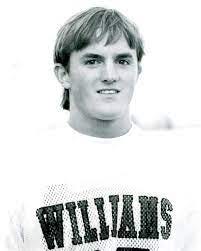

Charles Payson (Chase) Coleman III’s face tells you a few things. There is the jutting chin. In earlier pictures, his hair flops lightly over his forehead, he has the look of who he is.

In subsequent shots, as his prominence as one of the most successful hedge fund managers around grows, his locks are shorn, giving him the aspect of a Wall Street everyman. Still: that fresh faced appearance remains – it's hard to erase.

So why do we care? Because Coleman’s hedge fund, with it’s old school pedigree, is getting crushed due to massive bets on imploding tech stocks.

The market route has taken its share of scalps, with the bloodiest of the lot coming in speculative tech. Yes, Amazon, Alphabet and Facebook have swooned, but their losses pale in comparison to the wing and a prayer tech names that fill up the portfolio of Tiger Global.

According to The Financial Times, Tiger Global lost 44 percent in the first four months of this year. That translates to $17 billion, which wipes out two thirds of the fund’s returns since its 2001 inception.

These figures are extraordinary, hard to believe. Of course, we live in a time when hedge funds don’t hedge, they go all in, and can be volatile in the extreme. But to lose that amount of money and evaporate 20 years worth of gains in such a manner, well that takes some doing. See this recap by Robin Wigglesworth at the FT, including an apologetic letter from Tiger Global

Which brings us back to Coleman.

He is a Tiger cub, the top performer in the elite club of protegees blessed by legendary investor Julian Robertson. A died in the wool value maven, Robertson shut his doors in 2000, unable and unwilling to chase tech returns, to his detriment. Instead, he seeded a grouping of favored portfolio managers and sent them on their way.

Coleman was the most successful — by far. Prior to the recent carnage, AUM was $95 billion and he was ranked the 14th most successful manager of all time by a trade magazine. He is 46 years old. Those who got in early made many times their original investment.

Like others, he paid the price for crowding into the big momentum plays. Netflix. Shopify. Rivian. But check out some of the other names his fund is invested in. Snowflake. Cazoo Group. Dingdong. Ginkgo Bioworks. Mongodb. And my favorite: Toast (cloud based restaurant software) – down 75 percent over the past year.

This is outer periphery, last fumes of the bull market stuff.

A hedge fund falling on hard times is not unusual. We love when it happens.

But Coleman's meltdown delivers a purer form of schadenfreude. With his background, the fall has an epic quality.

Hedgies tend to be hard driving meritocrats. Modest backgrounds, elite brains and vast reserves of hunger. Stevie Cohen (Great Neck, Long Island) Ray Dalio and John Paulson (Queens, both).

As for Coleman, he grew up in Glen Head, on Long Island’s North Shore. Then Deerfield (double legacy), Williams (triple legacy and lacrosse, co-captain),

a starter job at Robertson’s Tiger. He was a friend of Robertson’s eldest son, Spencer. His father is a partner at the law firm Pillsbury, Winthrop, Shaw, Pittman. Mother: interior designer. He descends from the last Dutch governor of New York, Peter Stuyvesant (1647-1664).

Coleman is of a type. Clubbable, at his ease – perhaps a mid-level job at Brown Brothers Harriman, private client work at a boutique investment firm, a wills and trusts specialist at a modest law firm.

He is not of a type to achieve a net worth of $9 billion in 25 years. Marry a woman featured in the Born Rich documentary. Or invite select celebrities (Paris Hilton) to his $52 million co-op on 5th avenue to spray paint the walls before demoing the unit and combining it with two apartments on the floor above.

This is the kind of story that gets the juices flowing on a business desk. My editor at the New York Observer – Peter Kaplan (God rest his soul) – would have been all over it. He loved a comeuppance yarn with a touch of class edge. John fucking O’Hara, Landon.

Write it big and write it now.

I give him respect though. This is no Julian English, the well born, drink throwing anti-hero in Appointment in Samarra, whose life self-destructs in a period of three days. Coleman had balls. He ran toward fast money, not away for it.

There will be others that fail of course. The twenty year liquidity boom is over. Rates are going up, the Greenspan put is no longer. But the tech evangelists will be among the first. The crypto fanatics, Cathy Woods’ ARK ETF and now, Tiger Global.

In October 2000 (just a few months before Coleman started his fund), during the first months of the bursting of the Nasdaq tech bubble, I was at The Observer and did a story on the collapse of a technology fund — hoping to capture the excess and overreach of that era.

Ryan Jacob, the portfolio manager, was similarly boyish — and bullish.

A true believer in the soaring, profitless stocks that, in theory, would define the future of the web.

You might recognize a few of them. iVillage, Delia’s, AskJeeves, etc. His fund flew: from $22 million to $1 billion in two years. Then came the deluge. He was 31 years old when I interviewed him and getting pummeled, down 54 percent that year, with steeper losses to follow.

The funny thing was: there was no panic in him, or evidence of despair. Just incomprehension. He knew he was a smart guy, his investors celebrated him – now they were pulling their money out. This was not how it was supposed to end.

You come in every day and the market is down big, and you just say to yourself, ‘Man, this is bad.’ And then it’s down big again and again, until you just ask yourself, ‘My God, when is this going to stop?

Compelling stuff! Toast is indeed suitably named.